Written by Steve Andrews

Defying the Odds

If you’ve been following the markets and the economy over the past 18 months, you’re likely aware that nothing has gone according to plan. Most pundits assured us that the dramatic rate hikes from the Federal Reserve would drive the economy into the ground and a recession was all but certain by year-end.

Those fears never panned out. “Core” GDP, which excludes government spending, inventories, and international trade, grew at a 2.6% annualized rate in Q4 and finished the year up by 2.7%. Fear over the Fed was reduced further as GDP prices rose at a 1.5% annual rate in Q4 to finish the year up 2.6%. US consumers were responsible for the bulk of GDP growth last year, as they remained steadfast in spending, not only on necessities, but also on discretionary items like dining, travel, and entertainment.

Pundits at year-end grudgingly gave the economic performance its due. They were once again certain that the “surprise” accomplishment by consumers last year would leave them all but destitute for 2024, since “COVID Cash” has been all but depleted. We’re not so sure. The Fed has yet to release its report on Q4 Household Net Worth but, given the run-up in stocks and real estate at year-end, the report is expected to show that US household finances remain healthy.

Sector Dynamics

So, we find ourselves at the end of February with the economy again outperforming most expectations - driving stocks to record highs. Despite the showing, some have been dismissive, saying that it’s just a small number of stocks (the so-called MegaCap-8) that have driven the rise. And, while it’s true that, since this rally began back in October 2022, the S&P 500 has risen nearly 40%, fueled by the 80% rise in the Technology sector and a near-60% rise in the Communication sector, other key sectors like Financials, Industrials, Health Care, and Consumer Goods, etc., have also enjoyed a nice run.

The Future of Interest Rates

After a run like that, one worries that stocks may be getting ahead of themselves – especially since investors remain very focused on the Fed which has played the role of the bogeyman for investors for the better part of 2 years. The Fed’s pivot from rate hikes to eventual cuts removes a huge worry for investors, as seen in the recent sentiment surveys of small businesses, home builders, and consumers, but investors have shifted their angst to when the Fed will begin the rate cuts.

At the conclusion of its January 31 FOMC meeting the Fed stated that the "Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent." And, in his press conference following the announcement, Fed Chair Jerome Powell stated that incoming data has been in line with what the Fed would like to see in order to start the rate cut process. However, they would prefer to see the trend continue for a while longer to feel confident that they will not just hit their 2.0% inflation target - but will also be able to maintain it.

Surging Business Productivity

We tend to forget that US companies were forced to get lean and mean during the shutdowns and those adaptations have made them more resilient and stronger. Businesses large and small are benefiting from the new technologies that improve business efficiencies and, thus, productivity. US productivity rose 2.7% last year – well above the recent 5-year average rate of 1.9% and its long-term (since the end of World War II) trend of 2.1%. Productivity had been on the rise before the pandemic derailed its progress. Assuming this rebound continues with help from the boom in AI, robotics, and other technologies, we could see annual GDP growth returning to its long-term average growth of 3.1% (or better). Early estimates for Q1 GDP are coming in close to 3.0% growth (annualized) – a far cry from the expected slow start to 2024.

In Conclusion

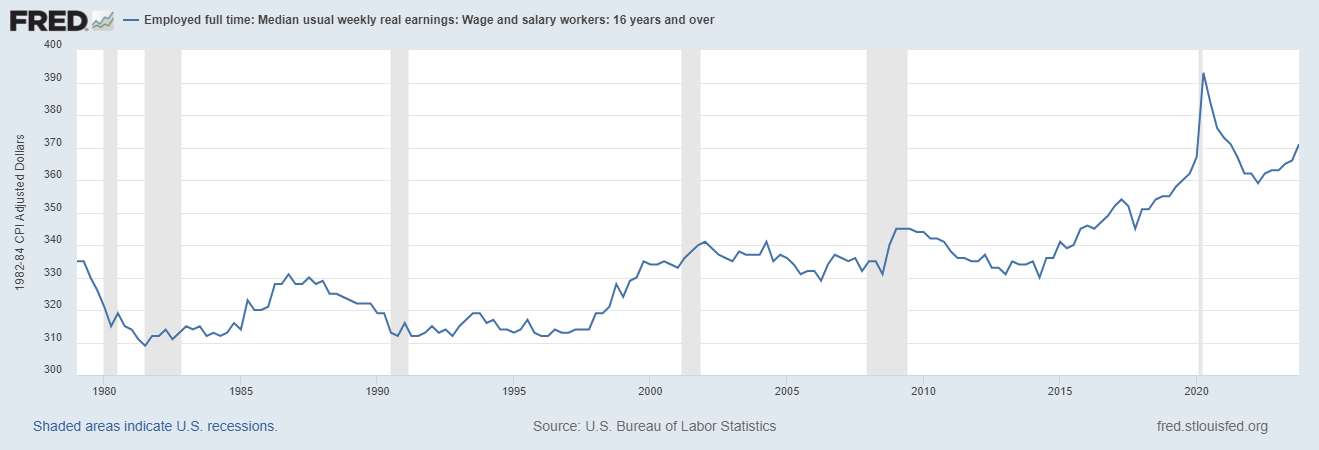

As we said at the outset, from an economic standpoint, little has gone according to plan but, since the plan called for economic recession, maybe that’s not so bad. Despite the healthy start to the year, the markets continue to operate in “musical chair” mode, where investors remain nervous and are poised to jump to safety at any perceived threat. In the background, however, economic fundamentals remain sound, with steady employment, rising wages, and household net worth supporting consumer spending. The downside to this, if you want to call it that, is that this will likely delay the first rate cut until mid-year or later, but the Fed, holding to its data-dependent approach to monetary policy, will act sooner if the economy should stumble.